Would you bet your company's entire quarterly profit on receiving just $3.42 for every kilogram of lost cargo? That is the cold, hard reality of sea freight liability in 2026. Many shippers believe they are protected by their carrier's policy, but there is a massive gap between being covered and being compensated. When comparing freight forwarder liability vs all-risk cargo insurance, the difference isn't just paperwork; it is the survival of your supply chain.

We get it. Logistics is already complex enough without decoding international conventions and SDR exchange rates. You want to move goods, not litigate claims for six months. This guide cuts through the bureaucratic noise to show you why carrier liability pays pennies on the dollar during "Acts of God" or General Average events. We will explain the "per-kilo" rule, compare current 2026 liability limits, and prove how all-risk insurance delivers the fast payouts and financial certainty your business demands. Stop gambling with your freight. Start protecting your margins.

Key Takeaways

- Stop trusting the "I'm covered" myth. Carrier liability is a legal shield for the forwarder, leaving your business with massive financial exposure.

- Master the math behind freight forwarder liability vs all-risk cargo insurance to avoid the "per-kilo" trap that pays pennies on the dollar.

- Secure your bottom line with all-risk protection that covers the full invoice value plus 10%, shielding your cash flow from unexpected disasters.

- Protect high-stakes shipments like reefer products with specialized coverage that handles temperature excursions where standard liability fails.

- Switch to a digital-first approach to get instant quotes and door-to-door transparency without the traditional insurance paperwork.

Freight Forwarder Liability vs All-Risk Cargo Insurance: The Great Disconnect

Imagine losing a container of high-value electronics in the middle of the Atlantic. You call your logistics partner. They mention their liability policy. You feel relieved. That relief is a mistake. A $100,000 mistake. Most shippers confuse professional liability with cargo protection. They aren't the same. Freight Forwarder Liability (FFL) is a policy designed to protect the freight forwarder from legal claims. It doesn't protect your balance sheet. It protects theirs.

When comparing freight forwarder liability vs all-risk cargo insurance, the disconnect is massive. FFL is third-party defense. It only pays out if you can prove the forwarder was legally negligent. All-Risk Cargo Insurance is first-party protection. It covers the full invoice value plus 10% to account for shipping costs and lost profit. It doesn't care who is at fault. It cares that your cargo is safe. Understanding the gap in freight forwarder liability vs all-risk cargo insurance is the difference between a recovered loss and a permanent financial hit.

The burden of proof is the ultimate dealbreaker for modern businesses. Under FFL, you are the investigator. You must prove the carrier failed in their duties or committed a specific error. This process is slow. It takes months. Most claims are rejected because "Acts of God," heavy weather, or third-party theft aren't legally the forwarder's fault. With All-Risk, the burden shifts entirely. The insurer pays the claim unless they can prove a specific, documented exclusion applies. It is speed versus bureaucracy. It is certainty versus a gamble.

The Core Difference: Liability vs. Ownership

Liability is about errors; ownership is about assets. If a storm hits your ship, the forwarder didn't make a mistake. They aren't liable. You lose everything. All-Risk insurance covers the goods themselves, regardless of negligence. It transforms a potential total loss into a simple administrative update. You don't have to sue your partner to get paid. You just file a claim, receive your payout, and keep your supply chain moving.

Why the 'All-Risk' Label Matters in 2026

Supply chains move at the speed of light in 2026. You don't have time for a six-month liability investigation. High-value electronics and reefer products need immediate financial certainty. All-Risk is the modern default because it eliminates the friction of finger-pointing. It provides door-to-door security, covering the "last mile" where current data shows most damage occurs. It is about total control in an unpredictable global market. Don't settle for a legal shield when you need a financial one.

Decoding Freight Forwarder Liability: The 'Per-Kilo' Trap

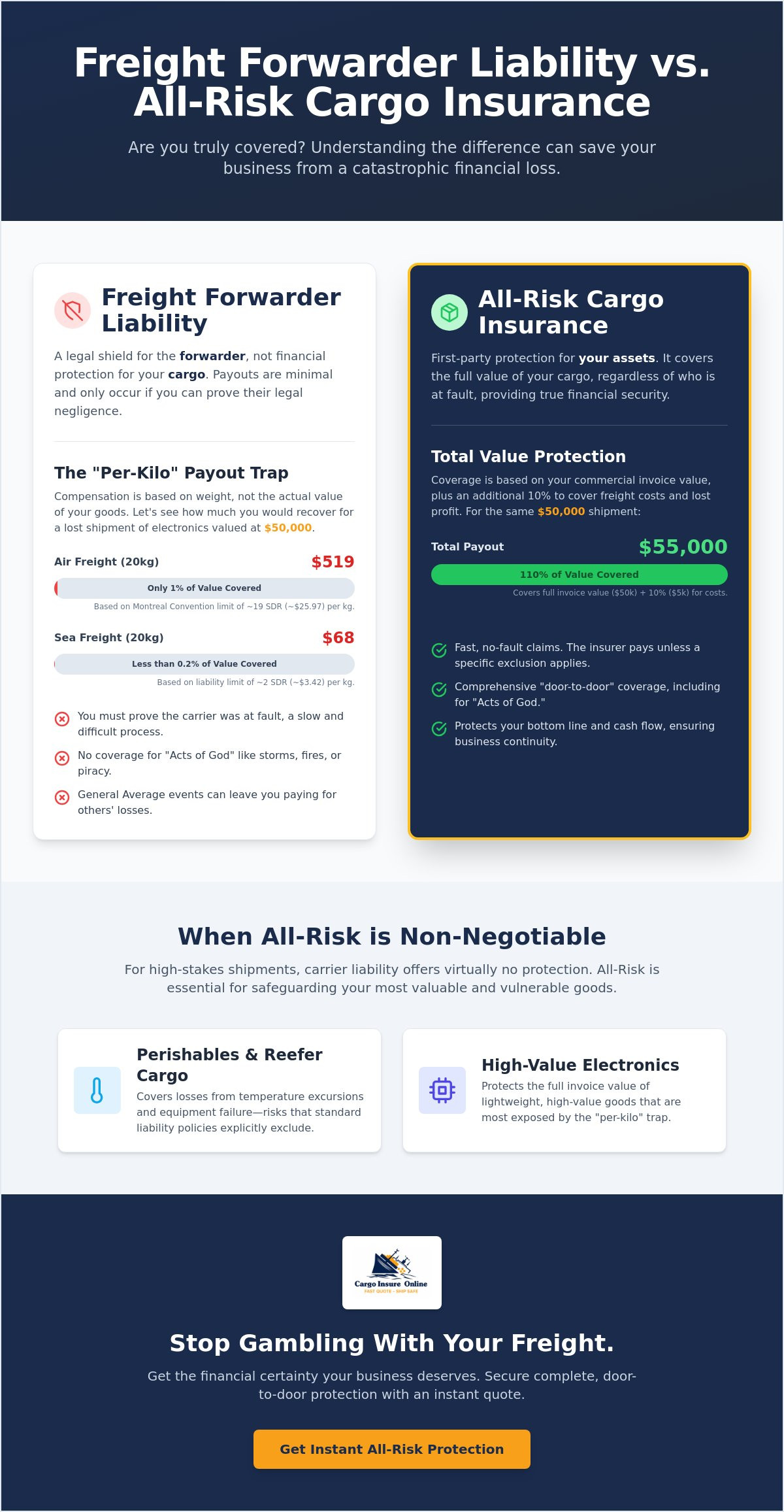

You ship a pallet of high-end tablets. The value is $50,000. The weight is 20 kilograms. If that pallet is crushed during a flight, you expect a full refund. Instead, you receive a check for $519. Welcome to the "per-kilo" trap. This is the most brutal reality of freight forwarder liability vs all-risk cargo insurance. While you see the value of your goods, international law only sees their weight. Your payout is decimated before the claim process even begins.

The math of loss is governed by Special Drawing Rights (SDR), a global reserve asset. As of June 2026, 1 SDR is worth approximately $1.37. When you rely on carrier liability, your compensation is capped by rigid conventions. For air freight, the limit is 19 SDR per kilogram. That equals roughly $25.97. If you are shipping lightweight, high-value electronics, you are essentially self-insuring 98% of your cargo's value without even knowing it. Avoid the math headache and secure your full invoice value with digital-first cargo insurance.

Sea freight is even more restrictive. Under the Carriage of Goods by Sea Act (COGSA), liability is often limited to just $500 per package. If an entire container is considered one "package" on the Bill of Lading, your recovery for a lost shipment could be less than the cost of the shipping container itself. These limits aren't suggestions. They are legal ceilings that protect carriers from the true cost of their mistakes. Understanding this gap in freight forwarder liability vs all-risk cargo insurance is vital for protecting your bottom line.

International Conventions You Can't Avoid

The Montreal Convention governs global air travel, setting the $25.97 per kilo limit mentioned above. For sea transport, the Hague-Visby Rules apply a pittance of 2.5 SDR per kilogram (about $3.42). If your cargo moves by road in Europe, the CMR Convention limits payouts to 8.33 SDR per kilogram (roughly $11.38). These rules are designed for the carrier's survival, not your recovery. They ensure the shipping industry stays profitable by shifting the financial risk of loss directly onto you.

Exclusions That Leave You Stranded

Even if the per-kilo math works in your favor, forwarders have a long list of "get out of jail free" cards. Insufficient packaging is the top reason claims are denied. If a forwarder can argue your boxes weren't sturdy enough, they pay zero. They also aren't liable for "Acts of God," meaning storms, fires, or even pirate attacks. Then there is General Average. If a ship's captain sacrifices some cargo to save the vessel, every shipper on that boat must pay to cover the loss. Without all-risk insurance, you aren't just losing your goods; you are paying for everyone else's too.

All-Risk Cargo Insurance: Total Protection for Modern Trade

Forget the $500 package limit. Forget receiving $26 per kilogram for your high-end drones. When you analyze freight forwarder liability vs all-risk cargo insurance, the winner is clear for any business that values its cash flow. All-risk coverage isn't a legal defense for a carrier. It is an asset protection plan for you. It covers the full invoice value of your goods plus an additional 10 percent. This "plus ten" is critical. It covers your freight costs and anticipated profit, ensuring a loss doesn't just mean a refund, but a total financial recovery.

The most powerful feature of all-risk protection is its door-to-door reach. Most damage happens during the "last mile" or at transfer points between trucks and ships. Standard carrier liability is often port-to-port or restricted to a specific leg of the journey. All-risk coverage follows your cargo from the moment it leaves the warehouse until it reaches the customer's doorstep. It bridges the gaps that carriers ignore, providing a continuous safety net across every border and every mode of transport.

You also eliminate the "blame game" entirely. Under a liability claim, you are a detective trying to prove a carrier failed. With all-risk insurance, you are a business owner getting paid. No proof of negligence is required. If the goods are damaged or stolen, the policy triggers. It is event-based, not fault-based. This is especially vital for General Average events. If a ship faces a disaster and cargo is sacrificed, carriers can hold your surviving goods hostage until you pay a cash bond. All-risk insurance pays that bond immediately. Your cargo is released. Your business stays operational.

What 'All-Risk' Actually Covers

Modern trade is messy. Rough handling, shifting containers, and pilferage are daily risks. All-risk insurance covers these physical threats plus environmental hazards like sea-water wash-over or freshwater damage from leaking containers. It accounts for non-delivery and total theft, scenarios where carriers often hide behind fine-print exclusions. It is the comprehensive answer to the unpredictability of global logistics.

The Speed of Digital Claims

Traditional insurance is slow. It involves mountains of paperwork and months of waiting. Cargo Insure Online changes that. By using a digital-first approach, we bypass the bureaucratic nightmare of liability investigations. You get instant quotes and automated claims processing. This speed is essential for e-commerce and high-value electronics where inventory turnover is everything. Stop waiting for a forwarder to admit they were wrong. Start getting your payouts in days, not months.

Risk Assessment for Perishables: When All-Risk is Non-Negotiable

Perishable goods don't have the luxury of time. When a refrigerator unit fails on a container in the tropics, you don't have months to argue about negligence. You have hours before your entire investment turns into compost. This is the highest-stakes arena for freight forwarder liability vs all-risk cargo insurance. In the cold chain, a minor technical glitch leads to a total loss. Without the right protection, that loss stays on your books forever.

Forwarders almost never accept liability for temperature excursions. Their contracts are riddled with exclusions for mechanical breakdown or "inherent vice." If a compressor stops at sea, the carrier will argue they performed "due diligence" and the failure was unavoidable. You are left holding a bill for ruined cargo and zero path to recovery. Reefer cargo insurance is the only way to ship perishables because it covers the event of spoilage regardless of who is at fault.

The spoilage clock is relentless. While a standard liability investigation drags on for half a year, your cash flow is frozen. You need a payout that matches the speed of your supply chain. Comparing freight forwarder liability vs all-risk cargo insurance reveals a simple truth: liability is a legal debate, but all-risk is a business solution. It ensures that even if the power goes out, your revenue stream stays on.

Specific Risks in Cold Chain Logistics

Cold chain logistics is a minefield of power failures and mechanical breakdowns. Standard carriers often hide behind the "delay" exclusion. If a ship is delayed by three days and your fruit spoils, the carrier pays nothing. They aren't responsible for the shelf life of your goods. Specialized insurance fills this gap. It covers the unique value of fresh cargo, protecting you from the financial fallout of transit delays and equipment failure. It turns a logistical nightmare into a manageable incident.

Protecting the Bottom Line for Importers

The cost-benefit analysis is undeniable. For high-value, time-sensitive goods, air freight insurance is a non-negotiable requirement. Consider the math. A $200,000 shipment of premium berries might weigh 4,000 kilograms. Under sea freight liability limits of approximately $3.42 per kilogram, your maximum recovery is around $13,680. If it falls under the COGSA $500 package rule, it is even worse. You lose nearly $190,000 in a single trip. Don't let a $500 liability cap destroy your business. Secure your shipment and get an instant cargo insurance quote today to lock in your margins.

Cargo Insure Online: Digital-First Protection in Seconds

The days of chasing carriers for pennies are over. Traditional insurance is slow. It is bureaucratic. It is frustrating. We built a better way. At Cargo Insure Online, we replaced the friction of the past with the speed of the future. You don't need a legal team to understand your coverage. You just need a solution that works as fast as your business does. We've simplified the complex so you can focus on growth, not claims.

Stop waiting for answers that never come. You can get instant quotes for sea freight insurance without the mountains of paperwork. Our platform delivers tech-driven transparency. There are no hidden clauses. There is no fine print designed to trap you. When you evaluate freight forwarder liability vs all-risk cargo insurance, the choice isn't just about money. It is about your time. We give that time back to you through automation and clarity that the old industry simply can't match.

We even empower the logistics providers themselves. Through our white-label power, forwarders can offer our high-tier All-Risk protection directly to their clients. This isn't just about selling a policy. It is about upgrading the entire shipping experience. The future of freight is seamless. It is automated. It is actually protective. We are moving the industry away from "liability reliance" and toward true asset protection. It is a new standard for a new era of trade.

Integration and Scalability

High-volume e-commerce and tech shippers need more than a basic policy. They need a partner that scales. Our API solutions integrate directly into your workflow, providing customized protection for drones, mobile phones, and high-value devices. This is why electronics shipping insurance requires All-Risk precision. A single damaged circuit board can cost thousands. You can't leave that kind of exposure to the "per-kilo" math of carrier liability. You need a digital shield that recognizes the actual value of your innovation and protects it instantly.

Your Next Move: Frictionless Coverage

The switch is simple. Stop hoping your carrier is at fault. Start knowing your assets are safe. Making the move from liability reliance to asset protection is the smartest decision you'll make this year. You can get a quote in under 60 seconds. It is fast. It is easy. It is the relief your supply chain has been waiting for. Don't let another shipment leave the warehouse without a safety net. Secure your shipment now with Cargo Insure Online and experience the 2026 standard for global trade protection.

Take Control of Your Supply Chain Risk

The choice is simple. You can continue relying on outdated "per-kilo" limits that leave your balance sheet exposed. Or you can embrace the certainty of modern asset protection. Understanding the gap between freight forwarder liability vs all-risk cargo insurance is the first step toward a resilient business. Carrier liability is a legal shield for them. All-risk insurance is a financial shield for you. It covers the full invoice value plus 10 percent; ensuring you never have to settle for pennies on the dollar again.

Stop waiting for the next disaster to find out if you are covered. Whether you are shipping high-value electronics or temperature-sensitive reefer products, you need protection that matches the speed of your trade. We provide global coverage for air, sea, and land with the transparency you deserve. No more hidden clauses. No more bureaucratic delays. Just instant digital quotes and total peace of mind. Stop gambling with your cargo, get an instant All-Risk quote now. Your cargo is the lifeblood of your company. Protect it with the sophistication it deserves.

Frequently Asked Questions

What is the main difference between carrier liability and cargo insurance?

Liability protects the carrier from you, while insurance protects your goods from the world. Carrier liability is a legal defense that only pays if you prove the forwarder was negligent. All-risk cargo insurance is first-party protection that pays out based on the event of damage or loss, regardless of who is at fault. It is the difference between winning a lawsuit and simply receiving a check.

How much does a freight forwarder's liability actually pay out?

Expect pennies on the dollar because payouts are based on weight, not value. In 2026, sea freight liability is limited to approximately $3.42 per kilogram, while air freight caps at roughly $25.97 per kilogram. When comparing freight forwarder liability vs all-risk cargo insurance, the math is brutal. If you ship a 10kg box of electronics worth $5,000, a liability claim might only net you $260.

Does all-risk cargo insurance cover everything?

It is the broadest coverage available, but it isn't a "blank check" for every scenario. It covers most physical loss or damage from external causes like rough handling, theft, or shipwrecks. However, it typically excludes inherent vice, which is natural decay, and damage caused by willful misconduct or extreme delays. The power of All-Risk is that the insurer must prove an exclusion applies to deny your claim.

Is freight forwarder liability insurance mandatory for shippers?

No, you aren't legally required to buy insurance, but you are legally exposed if you don't. Forwarders must carry liability insurance to stay in business, but that policy doesn't cover your financial loss. Skipping all-risk coverage means you are "self-insuring" the massive gap between the carrier's weight-based limit and your cargo's actual invoice value. It is a gamble that most modern businesses can't afford to take.

What is General Average and does cargo insurance cover it?

General Average is an ancient maritime law where everyone on a ship shares the cost if cargo is sacrificed to save the vessel. If a fire breaks out and your goods are safe but others were tossed overboard, you still have to pay. All-risk insurance covers these contributions and the necessary bonds. Without it, the carrier can legally hold your cargo hostage until you pay your share of the total loss.

How long does it take to get paid on a cargo insurance claim vs. a liability claim?

Insurance pays in weeks; liability takes months or even years. A liability claim involves a heavy legal investigation to determine fault, which often drags on for six to twelve months. Because all-risk insurance is event-based, the process is streamlined. Once you provide digital proof of the damage or loss, the payout is triggered. It is designed to keep your cash flow moving, not to keep lawyers busy.

Can I buy all-risk insurance if my forwarder already has a policy?

Yes, and it is the only way to ensure your assets are actually protected. The forwarder’s policy is there to defend them against your claims; it isn't a benefit for you. By securing your own freight forwarder liability vs all-risk cargo insurance solution, you become the direct beneficiary. You get the full invoice value plus 10 percent, bypassing the forwarder’s legal limits and bureaucratic hurdles entirely.

What are the common exclusions in all-risk cargo insurance?

The most frequent rejections stem from insufficient packaging or "inherent vice." If you ship fresh fruit that rots because it was already overripe, that is inherent vice and isn't covered. Other standard exclusions include loss due to war, strikes, or civil unrest, though these can often be added back with specific riders. Using a digital-first provider ensures these clauses are transparent, so you know exactly where your protection starts and stops.