The traditional cargo insurance claim process isn't just slow; it's a legacy system designed to stall your business. You've felt the pain of missing documents and the frustration of waiting up to 120 days for a carrier to settle. It's a bureaucratic marathon that drains your energy and your cash flow. Stop settling for "eventual" payouts and opaque evidence requirements. You deserve a system that moves as fast as your freight.

We agree that your time is too valuable for manual filing and endless follow-up emails. You need results, not excuses. This guide shows you how to navigate the cargo insurance claim process in 2026 with zero friction and maximum speed. We're breaking down the shift toward instant digital filing and providing a clear checklist of evidence to ensure your recovery is painless. You'll learn how to leverage digital documentation to speed up processing by 20% and maintain a healthy cash flow. It's time to turn a shipping disaster into a streamlined digital win.

Key Takeaways

- Ditch the paper trail and embrace a digital-first interaction that moves at the speed of your supply chain.

- Act fast in the first 24 hours to secure your goods and trigger the notification process without the usual friction.

- Build a bulletproof digital evidence stack to streamline the cargo insurance claim process and ensure a rapid payout.

- Avoid the common pitfalls of insufficient packaging and late filing that lead to instant claim denials.

- Stop chasing adjusters and start enjoying automated updates that keep your cash flow moving and your business growing.

Defining the Modern Cargo Insurance Claim Process

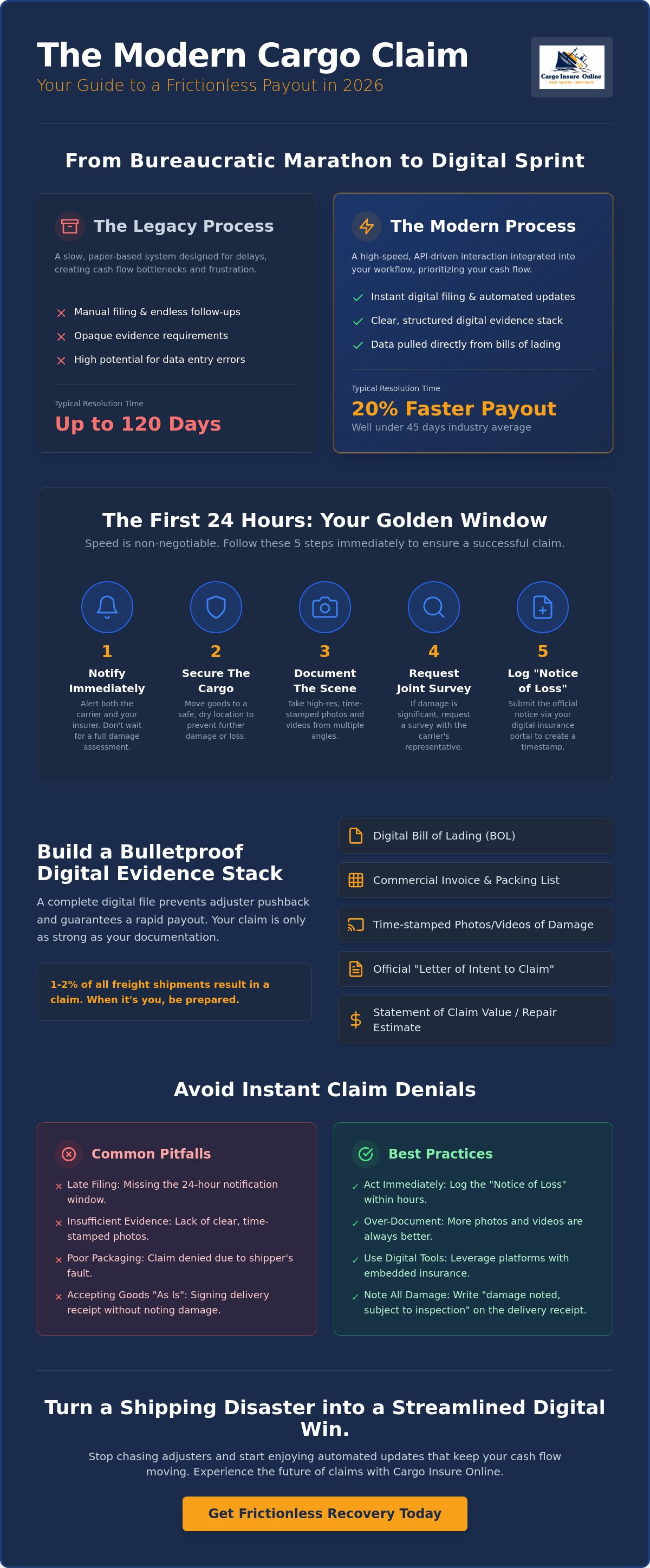

A claim is more than just a formal request for financial recovery; it's your business's safety net when physical logistics fail. It serves as the vital bridge between a crushed pallet or a lost container and the restoration of your balance sheet. In 2026, the cargo insurance claim process has evolved from a slow, manual marathon into a high-speed digital sprint. It's no longer a series of hopeful emails. It's a structured, API-driven interaction that prioritizes your cash flow over bureaucratic tradition.

The modern journey is linear and transparent. It moves rapidly through three critical phases: immediate digital notification, automated evidence gathering, and final financial payout. Approximately 1% to 2% of all freight shipments result in a claim. When you're part of that statistic, you don't need a lecture on policy terms. You need a frictionless path to recovery. High-performing digital platforms now ensure that claims filed with complete digital documentation process up to 20% faster than their paper-based ancestors, often settling well before the industry average of 45 days.

Why Traditional Claim Models are Failing

Legacy systems are the anchors dragging down your supply chain. Paper-based workflows create artificial bottlenecks, forcing you to wait for physical signatures and manual mail sorting. These outdated models rely on manual data entry, which is a breeding ground for errors and avoidable rejection rates. Traditional insurers often lack the real-time connectivity needed to verify losses as they happen. While federal regulations under 49 CFR § 370.5 give motor carriers up to 30 days just to acknowledge a claim, your business operates in seconds. You can't afford to wait months for a carrier to inform you they've declined a settlement offer after the 120-day resolution window.

The Shift to Embedded Insurance Solutions

The most significant disruption in 2026 is the integration of claims directly into your existing workflow. Claims are no longer a separate chore. They're a feature within your freight management software. This transition toward embedded insurance for freight companies automates the reporting phase by pulling data directly from your digital bills of lading. Instant data syncing removes the need for redundant status updates and "just checking in" emails. When your insurance is embedded, the system already knows the value of your goods, the route taken, and the parties involved. This connectivity allows for a cargo insurance claim process that triggers recovery the moment a loss is logged, turning a logistics failure into a seamless financial win.

The First 24 Hours: How to Start a Claim Correcty

Speed defines the outcome of your cargo insurance claim process. The moment you spot damage, the clock starts. You have exactly 24 hours to set the foundation for a successful payout. Hesitation leads to denial. Action leads to recovery. Follow these five non-negotiable steps to protect your investment:

- Step 1: Send an immediate notification to both the carrier and your insurer. Don't wait for a full assessment.

- Step 2: Secure the cargo in a safe, dry location to prevent further damage or loss.

- Step 3: Document the scene immediately using high-resolution digital media from multiple angles.

- Step 4: Request a joint survey if the estimated damage exceeds your policy's threshold limits.

- Step 5: Log the "Notice of Loss" through your digital insurance portal to timestamp your claim.

The Golden Hour of Evidence Gathering

The first 24 hours determine the success of your payout. This is your "Golden Hour." In 2026, digital timestamps on photos are non-negotiable. They prove the condition of the goods at the exact moment of arrival, leaving no room for insurer pushback. If you are a freight forwarder, this speed is even more critical. Understanding how cargo insurance for 3PL providers helps intermediaries act fast for their clients can be the difference between a happy customer and a lost account. You aren't just filing a report. You're building a digital wall of proof that prevents adjusters from questioning the timeline of the damage.

Notifying the Carrier: Protecting Your Rights

Notification isn't just a courtesy; it's a legal requirement to preserve your right to recovery. You must issue a formal "Letter of Intent to Claim" to the shipping line or trucker immediately. Under the Carmack Amendment, carriers have up to 30 days just to acknowledge your claim. That's too slow for your cash flow. Carrier liability is rarely enough to cover a total loss, often limited to pennies on the pound. By notifying them early, you preserve the right of subrogation for your insurance provider. This allows your insurer to pay you quickly and then chase the carrier for the funds later. If you want to skip the manual headache, start your next journey with a modern cargo insurance partner today. This ensures your financial restoration happens in days, not months.

The Digital Evidence Stack: What You Need for a Fast Payout

Paper is dead. Digital is the only way to ensure your cargo insurance claim process stays on the fast track. Forget the days of mailing original documents across borders and waiting for a physical signature. In 2026, your recovery depends on a "Digital Evidence Stack." This is a curated collection of cloud-based files that removes every ounce of doubt from an adjuster's mind. It's about providing undeniable proof in a format that's ready for instant verification.

Your evidence stack must be complete before you hit submit. Missing a single file can reset your payout clock. Focus on these four pillars of proof:

- Digital Bill of Lading (eBL) or Air Waybill (AWB): These digital twins prove the contract of carriage and the condition of the goods at pickup.

- Commercial Invoice: This isn't just a receipt. It's the definitive proof of the exact financial value of the damaged items.

- Packing List: Essential for verifying the quantity and weight of the shipment to identify shortages.

- High-Resolution Media: 4K photos and videos of the damage and the original packaging. If the box is crushed, the insurer can't claim it was an "inherent vice" of the product.

Special Requirements for High-Value Tech

High-value gadgets require high-precision proof. When filing electronics shipping insurance claims, serial numbers are your primary identifiers. Insurers need to know the exact unit that was lost or damaged. Document anti-tamper packaging and software seals for drones and mobile phones. If the hardware looks fine but won't boot, diagnostic reports provide the technical evidence needed for a transit-related damage payout. Don't just show the screen; show the system logs that prove internal failure.

Reefer and Temperature-Sensitive Data

Spoilage is often an invisible killer. You don't need a crushed container to have a total loss. Proving "thermal excursions" is the goal here. Download your data logger reports as soon as the doors open. These files show the exact temperature fluctuations during the carrier’s custody. Modern reefer cargo insurance relies on this telemetry to settle spoilage claims, even when there's no physical impact on the cargo. Data loggers don't lie, and they are your fastest route to a cold chain payout.

Why Most Cargo Claims Get Rejected (and How to Avoid It)

Rejection isn't an accident. It's usually the result of a small, avoidable technicality that legacy insurers use to protect their bottom line. Understanding the pitfalls of the cargo insurance claim process is just as important as knowing the steps. If you don't play by the rules of evidence and timing, your recovery ends before it begins. Most denials aren't about the damage itself; they're about how you handled the aftermath.

Insufficient packaging remains the absolute #1 reason for claim denial in global trade. Carriers and insurers expect your goods to withstand the "ordinary perils" of transit. If your pallets aren't double-stacked correctly or your bracing is weak, the insurer will categorize the loss as your fault. Beyond physical prep, timing is your biggest enemy. Filing outside the standard 3 to 7 day notification window is a guaranteed way to see a "claim denied" status. You must also watch out for "inherent vice," which refers to damage caused by the nature of the product itself, such as spontaneous combustion in certain chemicals or rust on untreated steel. Finally, never forget your duty to mitigate. You can't leave damaged electronics on a rainy dock and expect a full payout. You must take reasonable steps to prevent further loss once the initial damage is discovered.

The "Clean Receipt" Trap

Signing for a delivery as "received in good condition" can kill your claim instantly. This is the "Clean Receipt" trap. When you sign a Proof of Delivery (POD) without making notes, you're legally agreeing that the cargo arrived perfectly. This makes it nearly impossible to prove the carrier was at fault later. Always note "Subject to Inspection" or "Box Crushed" on the POD. If you discover concealed damage after the driver leaves, you have a much harder fight ahead. Digital photos with timestamps, as discussed in our evidence section, become your only lifeline in these disputes. Don't let a hurried driver talk you into a clean signature.

Inadequate Documentation and Missing Links

Precision is the difference between a payout and a headache. A common reason for friction in the cargo insurance claim process is a mismatch between your commercial invoice value and the insured amount. If these numbers don't align, the adjuster will flag the claim for a manual review, adding weeks to your timeline. Missing signatures on the Bill of Lading or incomplete packing lists create "missing links" in the chain of custody. You can eliminate these human errors by using a branded cargo insurance platform that uses automated validation to ensure every field is filled correctly before you hit submit. Ready to stop worrying about rejection? Start your journey with a digital-first insurance partner today and ensure your claims are built for success from day one.

Frictionless Recovery with Cargo Insure Online

The old way of handling claims was a black hole for your time and money. You sent emails into the void and waited weeks for a basic response. We've ended that era. Our digital portal transforms the complex cargo insurance claim process into a simple, 5-minute task. It's built for the speed of 2026 logistics. You don't have time to chase adjusters or decipher legalistic fine print. You need a partner that moves at the pace of global trade.

Our platform is designed to eliminate every friction point in your recovery journey. We provide a streamlined experience that focuses on results, not paperwork. Our system includes:

- 5-Minute Digital Filing: A guided, intuitive interface that ensures your claim is complete on the first attempt.

- Automated Status Updates: Real-time tracking of your claim's progress. Stop wondering where your money is and start planning your next move.

- Direct API Integration: Upload evidence directly from your warehouse or freight management system. No manual downloads or redundant data entry required.

- Rapid Payout Technology: We prioritize your cash flow. Our system is engineered for the fastest financial restoration in the industry.

The Tech-Driven Advantage

We don't just process claims; we accelerate them. While traditional insurers rely on manual reviews that take weeks, we use AI to validate your documentation in seconds. Our "Zero Paperwork" digital claim engine cross-references your digital bills of lading and commercial invoices instantly. This transparency builds trust and removes the guesswork from the equation. 2026 logistics leaders choose us because we provide more than just a policy. We offer high-speed risk management that protects your reputation and your bottom line. We've replaced the administrative chore with a seamless, positive experience that gives you total control over your financial recovery.

Ready to Experience Hassle-Free Shipping?

Don’t wait for a major loss to realize your current insurance is a relic of the past. If your insurer still asks for physical copies of your evidence stack, they're holding your business back. Protect your high-value assets with a modern, digital-first policy that respects your time and your intelligence. Whether you're moving high-value electronics, drones, or temperature-sensitive reefer products, we have the specialized coverage you need. You can get an instant quote and secure your next shipment in minutes. It's time to experience a cargo insurance claim process that actually works for you. Join the modern era of logistics and secure your business today.

Master Your Logistics Recovery in 2026

Logistics in 2026 doesn't wait for slow paperwork or physical signatures. You've seen how the modern cargo insurance claim process has shifted from a manual chore to a data-driven sprint. Success starts with mastering the "Golden Hour" of evidence and ends with a frictionless payout. Stop letting legacy insurers hold your cash flow hostage with outdated rejection traps and opaque response times. You need a partner that matches your operational speed. It's about moving from administrative frustration to financial relief in minutes.

By focusing on a bulletproof digital evidence stack and acting within that critical 24-hour window, you eliminate the friction that stalls most recoveries. Powered by CIO Sphere Inc. technology, our digital-first claims engine is built for the high-stakes world of global trade. We provide global coverage for high-value electronics and reefer goods, ensuring your assets are protected anywhere on the map. It's time to leave the bureaucracy behind and embrace a smarter way to manage risk. Ship with confidence; get your instant cargo insurance quote now. Your supply chain is ready for a faster, more transparent future.

Frequently Asked Questions

How long does the cargo insurance claim process take?

Digital claims move much faster than legacy paper trails. While federal regulations allow carriers up to 120 days to resolve a dispute, a digital-first cargo insurance claim process often settles in around 45 days. Complete documentation is the key to speed. By using API-driven platforms to sync evidence instantly, you can cut processing times by 20%. It's about removing manual review bottlenecks and getting your cash flow back on track.

Can I file a claim if I don’t have an All-Risk policy?

You can still file a claim, but your recovery depends on proving a specific "Named Peril" occurred. Unlike All-Risk coverage, which covers most losses unless excluded, basic policies only pay out for events like shipwrecks, fires, or plane crashes. This puts the burden of proof on you. It's often a steeper uphill battle. We always recommend All-Risk to ensure your high-value cargo has the broadest possible protection against the unexpected.

What happens if the damage is only discovered after delivery?

Concealed damage claims are possible but require immediate action. You typically have a very narrow window, often just 3 days, to report damage found after the driver leaves. This is where your digital evidence stack saves the day. Use high-resolution photos with clear timestamps to prove the damage happened during transit, not in your warehouse. Without this proof, insurers might argue the loss occurred after you took official custody of the goods.

Do I need to hire a marine surveyor for every claim?

You don't need a professional surveyor for every minor scratch. Most digital platforms allow you to self-document smaller losses using photos and videos. However, if the damage exceeds a specific threshold, usually several thousand dollars, a joint survey becomes essential. This involves an independent expert verifying the loss on-site. It adds a layer of authority to your claim. Check your specific policy for the exact dollar amount that triggers a mandatory survey.

Will my claim be rejected if the carrier was not at fault?

Not if you have the right coverage. A modern cargo insurance claim process under an All-Risk policy focuses on the loss itself, not just carrier negligence. Even if the damage resulted from an "Act of God" like a hurricane, you're covered. This is the biggest advantage over relying on carrier liability. Carriers have many legal defenses under the Carmack Amendment to avoid paying. Your insurance bridges that gap, ensuring you get paid regardless of carrier fault.

How much does it cost to file a cargo insurance claim?

Filing a claim doesn't cost an upfront fee, but you should account for your policy's deductible. This is the amount you agree to pay out of pocket before the insurance coverage kicks in. Some specialty policies for high-value electronics or reefer goods may have different deductible structures. Beyond the deductible, the only "cost" is the time spent gathering evidence. Digital portals minimize this by turning hours of manual paperwork into a 5-minute digital task.

Can I claim for lost revenue due to shipping delays?

Standard cargo insurance typically covers physical loss or damage, not purely financial losses from delays. If your shipment arrives late but intact, a basic policy won't pay for your missed sales or lost revenue. However, some advanced endorsements can be added to cover "consequential loss." Always check your policy's specific terms. If your business model is highly sensitive to time, you'll want to discuss specific delay-related protections with your insurance provider.

What is the difference between a claim and a carrier grievance?

A claim is a formal request to your insurance provider for financial recovery under your policy. A carrier grievance is a direct dispute with the shipping company. While you must notify the carrier of damage to preserve your rights, chasing them for payment is often a losing battle. They have strict liability limits and long legal windows. Your insurance claim is the faster, more reliable route to getting your money back and maintaining your cash flow.