What if your carrier’s insurance isn't just insufficient, but completely irrelevant when a claim hits your desk? With the U.S. Supreme Court’s 2026 ruling in Montgomery v. Caribe Transport II, the legal shield for brokers has evaporated. You’re now directly exposed to negligent hiring claims. You already know the headache of manual quoting and the anxiety of carrier policy exclusions. Finding reliable cargo insurance for freight brokers shouldn't feel like a relic of the 1980s. No more chasing paper. No more manual quotes. Just high-speed protection.

You deserve a strategy that keeps pace with your growth. This article reveals how to eliminate liability gaps and protect your brokerage with frictionless, high-speed cargo insurance solutions. We are breaking down the shift from contingent policies to all-risk coverage and showing you how digital automation transforms risk management into a competitive advantage. It’s time to stop reacting to claims and start preventing them with a shield built for the modern era.

Key Takeaways

- Stop relying on carrier liability. Learn why "per-kilo" rules pay pennies and how to secure real protection for every shipment.

- Upgrade your defense. Discover why modern cargo insurance for freight brokers is shifting from slow contingent plans to high-speed, all-risk coverage.

- Protect high-value tech. Uncover the hidden exclusions in electronics, reefer, and drone shipments that leave your brokerage exposed.

- Audit for growth. Follow a clear two-step strategy to vet carriers for compliance and identify your most vulnerable freight lanes.

- Move at digital speed. Master a frictionless insurance approach that delivers instant quotes and eliminates manual administrative friction.

Why Carrier Liability Isn’t Your Safety Net

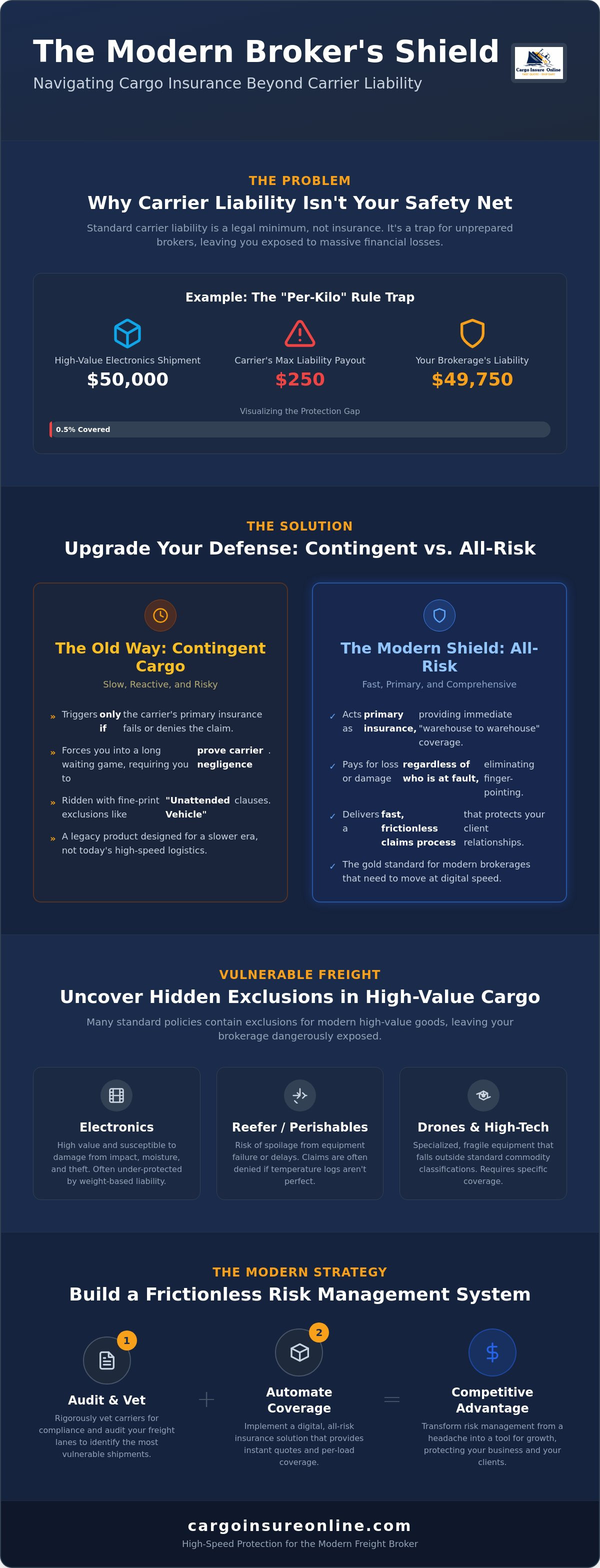

Think carrier liability is your safety net? Think again. It’s not insurance; it’s a legal minimum. Many brokers assume that a carrier’s Certificate of Insurance (COI) covers the load. It doesn't. Standard carrier liability is a limited legal obligation, often governed by the Carmack Amendment, which allows carriers to cap their financial exposure. Standard carrier liability is not a substitute for robust cargo insurance for freight brokers. It’s a trap for the unprepared.

The "Per-Kilo" rule is the first place brokers get burned. Under standard liability, a carrier might only be responsible for $0.50 per pound or a set amount per kilo. If you’re moving a pallet of high-end electronics weighing 500 pounds but valued at $50,000, the carrier’s legal payout might only be $250. That’s not a settlement; it’s an insult. You are left explaining a massive financial loss to a frustrated shipper.

Exclusions make the situation even worse. Carriers can walk away from claims citing "Acts of God," improper packing, or even certain types of driver negligence. If a tornado flips a trailer, the carrier isn't liable. If the shipper’s warehouse team used the wrong tape, the carrier isn't liable. When these claims are denied, the shipper doesn't blame the weather; they blame you. Without dedicated cargo insurance for freight brokers, you are the easiest target for a lawsuit.

The Gap Between Liability and Full Protection

The Carmack Amendment was designed to protect carriers, not brokers or shippers. It creates a high bar for proving carrier fault. Relying on a carrier’s COI is a high-stakes gamble because those policies can be cancelled, exhausted by other claims, or filled with "named peril" exclusions that you never see. To understand the roots of these protections, one should look at Marine insurance principles, which dictate how risk is distributed across global trade lanes. The liability gap is the financial difference between a carrier’s legal limit of liability and the actual replacement value of the cargo.

The Cost of Being Unprotected in 2026

The financial hit goes beyond the cargo value. Even if a court eventually finds you aren't liable, the legal fees to reach that verdict can bankrupt a small brokerage. In 2026, the rise in "nuclear verdicts" means that even minor disputes can escalate into multi-million dollar legal battles. Beyond the cash, your reputation is on the line. One denied claim can lose you a Tier-1 shipper forever. Shippers want partners who provide solutions, not excuses. You can learn more about closing these loopholes in our guide on Freight Insurance Coverage: The 2026 Guide to Frictionless Shipping. Speed and clarity are your only real defenses.

Contingent Cargo vs. All-Risk: Decoding Broker Protection

Contingent cargo is the industry's old security blanket. It’s a legacy product designed for a slower era. This "if-then" policy only triggers if the carrier’s insurance fails first. It forces you into a waiting game. You have to prove the carrier was legally liable before your own policy even considers the claim. In a high-speed logistics environment, this delay is a business killer. Modern cargo insurance for freight brokers should be a primary shield, not a secondary "maybe."

The distinction between who pays first is critical. Primary insurance covers the loss immediately. Contingent insurance waits for the carrier's policy to exhaust or deny coverage. While FMCSA broker requirements mandate a $75,000 surety bond, that bond is for financial responsibility, not cargo protection. It won't help you when a $200,000 load disappears. You need a solution that moves as fast as your freight.

The Pitfalls of Traditional Contingent Policies

Traditional contingent policies are riddled with fine-print traps. The most notorious is the "unattended vehicle" exclusion. If a driver leaves the truck for a meal and the cargo is stolen, many contingent policies simply won't pay. Legal Form policies are even worse because they lack a robust "Duty to Defend" clause. This means you are responsible for your own legal fees until you can prove you weren't at fault. Broad Form coverage is a slight improvement, but it still requires you to prove carrier negligence, which can take months of litigation. Don't let your brokerage get stuck in the finger-pointing phase.

Why All-Risk is the Future of Brokerage

All-Risk is the gold standard for a reason. It provides "warehouse to warehouse" coverage regardless of who is at fault. If the goods are damaged, the policy pays. This is especially vital for electronics shipping insurance, where internal component damage is often hard to attribute to a specific moment of negligence. All-Risk removes the friction from the claims process. It settles losses quickly, keeping your shippers happy and your cash flow steady. It transforms insurance from a bureaucratic hurdle into a competitive advantage. You can explore frictionless all-risk options here to see the difference for yourself.

Choosing All-Risk means choosing certainty. It eliminates the need to audit every carrier's specific policy exclusions because your primary coverage is already in place. This is the ultimate cargo insurance for freight brokers who value their time and their reputation. Stop playing defense and start scaling with a primary policy that actually has your back.

Hidden Risks in Modern Logistics: Electronics, Reefer, and Drones

Moving a load of lumber is straightforward. Moving a trailer full of high-end smartphones or specialized drones is a different game entirely. In 2026, the complexity of cargo has outpaced the simplicity of legacy insurance. Standard cargo insurance for freight brokers often treats every load with the same broad brush. This approach leaves you dangerously exposed when high-value assets hit the road. You need a strategy that understands the nuance of modern freight.

Cyber risk is the new frontier of brokerage liability. Fictitious pickups and identity theft have become sophisticated operations. A carrier might look perfect on paper, but if they are a digital ghost, your cargo is gone the moment it's loaded. Standard policies often exclude "voluntary parting" of goods, meaning if you give the load to a fraudster, you aren't covered. High-speed, digital insurance partners use real-time data to spot these red flags before the truck even arrives.

Safeguarding High-Value Tech and Electronics

Theft-prone cargo like smartphones and high-precision drones requires more than just a higher limit. Standard $100,000 per-load limits are a joke when a single pallet of electronics can exceed $1 million in value. You need "Full Value" coverage that reflects the actual replacement cost, not just a weight-based estimate. High-value tech requires specific "theft prevention" clauses in a policy to ensure that minor procedural errors don't void your entire claim. Don't let a legacy policy dictate your tech shipping success. Secure coverage that scales with the value of the innovation you move.

The Fragility of the Cold Chain

The cold chain is only as strong as its weakest link. If a reefer unit loses power or a driver forgets to set the correct temperature, the entire load can become a total loss. Most basic policies have a gap between "mechanical breakdown" and "driver error." You need a solution that covers both. Spoilage and contamination are the hidden killers of brokerage margins. Beyond the physical goods, you face disposal fees and environmental fines. Learn how to bridge these gaps in our guide to Reefer Cargo Insurance: The Modern Guide to Cold Chain Protection. Modern sensors and digital cargo insurance for freight brokers now work in tandem. They provide the real-time visibility needed to mitigate losses before they become catastrophic. Stop guessing and start protecting your temperature-sensitive lanes with precision.

Building a Frictionless Insurance Strategy for Your Brokerage

Legacy brokerage models are hitting a wall. Stop chasing paper trails and start automating your defense. Modern cargo insurance for freight brokers isn't a policy you buy once a year and forget. It’s an agile, per-load strategy that eliminates gaps before they cost you a client. You need a workflow that moves as fast as a digital freight matching platform. Efficiency is your only path to scaling in 2026.

Building this shield requires a tactical shift. Follow these five steps to modernize your brokerage:

- Step 1: Audit your current carrier vetting process for real-time insurance compliance.

- Step 2: Identify your high-exposure lanes, specifically looking for high-value electronics or reefer goods.

- Step 3: Move from rigid annual aggregate policies to flexible, per-load digital options.

- Step 4: Integrate insurance into your TMS or workflow via API for instant coverage.

- Step 5: Partner with a digital-first intermediary like Cargo Insure Online to handle the heavy lifting.

Modernizing Your Vetting Workflow

A Certificate of Insurance (COI) is a snapshot of the past. It doesn't tell you if a policy was cancelled yesterday or if a specific exclusion voids your current load. Vetting isn't a one-time event; it’s a continuous requirement. You must set minimum standards for carrier insurance that specifically protect your contingent interests. This includes verifying "all-risk" status and checking for "unattended vehicle" clauses. For land-based moves, understanding Inland Marine Cargo Insurance: The Modern Shield for Land Logistics is essential for closing the gaps that standard liability leaves wide open. Don't gamble on a carrier’s word. Verify their coverage in real-time to keep your brokerage safe.

The Power of Digital Integration

Waiting 24 hours for a quote is a death sentence in 2026 brokerage. If you can't price the insurance instantly, you can't bid on the load with confidence. Automated quoting allows you to secure high-value freight while your competitors are still playing phone tag with brokers. Integrating cargo insurance for freight brokers into your existing tech stack via API removes the manual friction of data entry. This isn't just about protection; it’s about growth. White-label solutions even let you offer insurance as a value-add service to your shippers, turning a cost center into a professional advantage. You can get your frictionless quote now and see how speed transforms your operations. Stop reacting to the market and start leading it with a digital-first approach.

How Cargo Insure Online Empowers Modern Brokers

Logistics moves at the speed of data. Your insurance should too. Cargo Insure Online (CIO) isn't just another provider; it’s a digital-first partner designed to crush the administrative friction that holds brokers back. We provide the cargo insurance for freight brokers that 2026 demands. It’s about more than just a policy. It’s about empowering your team to bid on high-stakes loads without hesitation. You get the protection you need in the time it takes to send a text.

No more endless email threads. No more guessing at coverage limits. CIO delivers results where legacy brokers deliver delays. We focus on the high-value sectors that others find too complex.

- Instant quotes: Stop the back-and-forth and get covered in seconds.

- Specialized expertise: Deep protection for electronics, reefer, and high-value freight.

- Global reach: Whether it’s air freight insurance or domestic trucking, we cover it all.

- Frictionless claims: A digital-first process designed to get you paid, not delayed.

The CIO Advantage: Speed, Tech, and Transparency

No more paperwork. No more waiting. Just instant, intelligent coverage. Our platform acts as a sophisticated ally for high-performing brokers who refuse to be slowed down by 1980s era bureaucracy. The digital-first promise means transparent pricing with zero hidden jargon. You get the clarity you need to make fast decisions. We’ve mastered the complexities of global trade and simplified them into a single, high-speed user journey. It’s professional authority meets playful enthusiasm.

Scaling Your Business with White-Label Solutions

Growth requires more than just moving loads; it requires adding value. With CIO, you can launch your own branded insurance engine. This transforms cargo insurance for freight brokers from a necessary expense into a powerful competitive tool. By offering White Label Cargo Insurance, you provide your shippers with seamless protection under your own brand. You become the one stop shop they trust for every high-value shipment. This isn't just about insurance. It's about building a modern, tech-forward brand that shippers can't ignore. Move faster, protect better, and scale bigger with a partner that values your time as much as you do.

Future-Proof Your Freight Strategy

Legacy insurance is a bottleneck. Modern logistics is a race. You've seen why standard carrier liability is a trap and why contingent policies leave you exposed. The shift to all-risk, per-load coverage isn't just a trend; it's a survival requirement for the modern era. By automating your vetting and integrating digital protection, you transform a required chore into a competitive edge. No more paper trails. No more waiting. Just instant, intelligent coverage.

Cargo Insure Online delivers the high-speed cargo insurance for freight brokers that keeps your business moving. Whether you're securing $1M+ electronics loads or managing complex reefer chains, our platform provides the specialized protection you need. We offer instant digital quotes for air, sea, and land, alongside white-label solutions that empower your brand. Don't let legacy friction stall your growth. Shield your brokerage with instant, frictionless cargo insurance today. Your future is frictionless. Let's get moving.

Frequently Asked Questions

Does a freight broker really need cargo insurance if the carrier is insured?

Yes, you absolutely need it. Carrier policies are riddled with exclusions like "Acts of God" or "unattended vehicle" clauses that can leave you exposed. Relying solely on a carrier's COI is a high-stakes gamble. If their insurer denies a claim, your shipper will look to you for the full replacement value. Dedicated cargo insurance for freight brokers ensures you have a primary shield that pays regardless of carrier policy failures.

What is the difference between Legal Form and Broad Form contingent cargo insurance?

Legal Form is the most restrictive option. It only pays if you are found legally liable for the loss, which is a high bar to clear in court. Broad Form is a significant upgrade. It triggers when the carrier’s primary insurance fails to pay for a covered loss. While Broad Form is better, it still lacks the "warehouse-to-warehouse" certainty of an All-Risk policy.

Can I buy cargo insurance for just a single high-value load?

Yes, you can. Modern digital platforms allow you to secure coverage on a per-load basis. This is ideal for high-value electronics or specialized reefer goods that exceed your annual policy limits. You don't have to pay for a massive aggregate policy when you only need protection for a specific, high-risk lane. It’s about paying for exactly what you move, when you move it.

What happens if a carrier’s insurance policy has an exclusion for the cargo I’m moving?

The claim gets denied instantly. If the carrier’s policy excludes specific items like mobile phones or drones, their insurer won't pay a cent. This creates a massive liability gap. Without your own cargo insurance for freight brokers, you are financially responsible for the total loss. This is why verifying specific exclusions is more important than just checking the total coverage limit on a COI.

How does All-Risk cargo insurance differ from standard carrier liability?

All-Risk provides comprehensive coverage for any physical loss or damage unless the cause is specifically excluded. In contrast, standard carrier liability is often capped by weight, sometimes paying as little as $0.50 per pound. All-Risk pays based on the full invoice value of the goods. It removes the need to prove negligence, focusing on the result rather than the fault.

What are the FMCSA bond requirements for freight brokers in 2026?

As of 2026, the FMCSA requires all freight brokers to maintain a $75,000 surety bond (BMC-84) or trust fund (BMC-85). This requirement ensures financial responsibility for payments to motor carriers and shippers. If your bond falls below this threshold, your brokerage authority can be suspended within seven days. This bond is mandatory, but it does not replace the need for actual cargo insurance.

How long does the cargo insurance claim process take with Cargo Insure Online?

Our process is built for speed. While traditional insurers take weeks to investigate, our digital-first approach focuses on rapid documentation and frictionless payouts. We eliminate the legacy "finger-pointing" phase by using clear, data-driven evidence. Our goal is to resolve claims in days, not months. We understand that your cash flow and shipper relationships depend on a fast, transparent resolution.

Can I integrate cargo insurance quotes directly into my brokerage TMS?

Yes, integration is seamless. You can use our API to pull instant quotes directly into your existing TMS or workflow. This eliminates manual data entry and allows your team to secure coverage without leaving their primary operating screen. It’s about creating a frictionless environment where insurance is a value-add, not an administrative chore. Stop the back-and-forth and start automating your risk management.